Swiggy: A Fine Dine or a Waste of Time?

Unpacking my thoughts on Swiggy being a sweet deal or an overpriced meal

Over a month ago Swiggy - ironically - through its confidential filing route announced its plan to join the bourses with an IPO of INR 10,414 Crore. As a Swiggy loyalist & a sucker for a burger every Sunday night, I decided to immerse myself in the noise on Dalal Street and the murmurings of the VC world to try and forge an opinion on what this signifies.

Swiggy is a food-tech delivery platform founded in 2014 and headquartered in Bengaluru, Karnataka. Swiggy is eyeing an IPO through a mix of new issuances and offer for sale from existing investors.

In an attempt to spruce up its operations, Swiggy has been optimizing its workforce and unit economics:

Swiggy reduced its workforce by 6% a year ago. Budget cuts have been pervasive in the Company with muted increments and longer working hours

Involvement of the senior leadership team at the tactical & operational levels

Working towards a more restaurant-centric relationship through periodic engagements & meetings

Closed its Meat Marketplace and delivery subscription service for milk, groceries, etc; Sold its cloud kitchen business through a share swap, resulting in a stake at Kitchens@

Focus on outcome advertising through its cost-per-click service (>90% margin)

This has yielded results with its food delivery business attaining profitability in March 2023, and its operating revenue growing by 44.9% to INR 8,264.6 Crore in FY 23.

In the quick commerce vertical, Swiggy Instamart is the incumbent with a presence in more than 25 cities and a reported revenue of INR 3,221.4 Crore in FY 23. With quick commerce companies having a strong bargaining power with brands, Swiggy has been actively improving its product assortment & customer experience.

However, with all these strides, Swiggy has ceded ground to Zomato and other players in an industry that is quickly evolving and steering away from being a duopoly.

Let me take you through my latest binge on what’s possibly holding me back from pressing the ‘Place Order’ button:

Offer for Sale

Swiggy was last valued at USD 15.1 Billion by Baron Capital in June 2024 - a 25% rise - and has seen 4 valuation markups since its last funding round in early 2022. This came after Swiggy had filed its pre-IPO papers in May.

However, a few notable backers like Prosus and Softbank want to sell a significant portion of their stake before the IPO debut. Even though this can be seen as a natural progression for VC & PE firms, it also creates a perception of the Company being overvalued, now at a value close to Zomato.

Swiggy has reportedly said the IPO is the ultimate exit strategy for most investors, particularly late-stage ones.

The company is also reportedly doing a pre-IPO round of INR 700 Crore to HNI’s and anchor investors to purchase its shares at a 20% mark-down from its pegged valuation (currently valued between USD 9-9.5 Billion in the grey market). This potentially serves as a testimony to what institutions believe the business's intrinsic value is worth.

Current Financial Performance

According to Entrackr, Swiggy recorded INR 5,476 Crore revenue from operations and INR 1,600 Crore loss during the first three quarters of FY 24.

Swiggy's overall Financials/Performance is not public but it has reportedly lost a considerable share to Zomato in the food delivery segment despite being the first to enter it.

Zomato has seen 4 consecutive quarters in the green posting a consolidated profit of INR 175 crore in Q4 FY 23, a 28% increase over the previous quarter. Besides recent volatility, Zomato has seen its stock price recover, reaching an all-time high of INR 205 on May 10th, 2024.

According to a Bernstein Report:

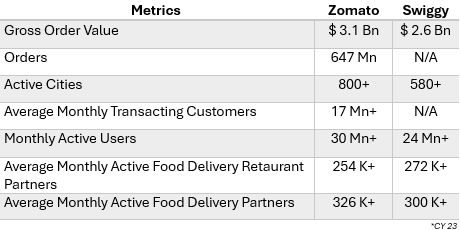

Zomato has a 54% market share in Gross Merchandise Value (GMV) terms in the food delivery business compared to Swiggy’s 46%. The food delivery contribution margin also sees a healthy expansion due to a higher Average Order Value (AOV)

In the Monthly Active Users (MAU) Ratio, Swiggy has seen a fall with a 40-60 split to Zomato due to the latter’s deeper penetration in smaller cities. In 2023, Zomato saw 41 new million downloads while Swiggy saw a little under 30 million. Being a listed company could fuel this growth as Zomato may have a better customer recall value

Zomato has been better at execution on all fronts: The take rate of GMV has risen to just below 20%, and it has actively been leveraging its revenue levers - Platform fees, advertisements & loyalty fees to improve its performance. Zomato also reports a higher EBITDA margin than its global peers

Quick Delivery Segment

Amidst the controversy, 10-minute delivery seems to be here to stay and has emerged as the key driver of profitability for food delivery companies.

Swiggy’s Instamart has been a laggard in the space, holding 37-39% after Blinkit which has north of 40% from a GMV perspective. Blinkit boasts a wider catalogue, wider penetration through cities and dark stores & overall stronger execution.

Swiggy has made a significant investment of almost USD 700 Million - trying to build a grocery delivery arm from scratch. However, it’s burned over INR 1,000 Crore in the first 9 months of FY24 and internal reports indicate it will continue to see negative EBITDA figures till FY 26.

Blinkit turned adjusted EBITDA positive in March 24, with revenues rising by 19% to INR 769 Crore in Q4 FY24 due to a healthy growth in the number of orders and AOV during the three months.

With the quick commerce industry in the hyper-growth stage, Goldman Sachs valued Blinkit at USD 13 Billion, making its contribution to Zomato’s market capital larger than its food delivery business.

With the potential this vertical promises, conglomerates like Reliance, Tata and Flipkart are entering the ring, and intensifying the competition.

Role of Gig Workers

With an expanding delivery fleet boasting almost 7 Lakh+ delivery “partners”, Swiggy (along with other platforms) still makes the news for not providing adequate salaries & other benefits to their gig delivery workers.

As fuel prices take away 1/3rd of earnings and rising inflation, Swiggy (& other platforms) have had to put out multiple fires as it precariously tries to balance the payment terms to its delivery workers and not pass rising costs to its customers.

Even though there is an increased AOV and frequency witnessed, these profits have not been proportionately shared with the delivery partners.

Through its renewed focus on profitability over expansion, Swiggy has gamified the insurance it provides to its delivery partners, based on limited tiers and the whims of its customers.

With growing socio-economics awareness and calls for a more robust set of laws protecting blue-collar workers, Swiggy must realize its obligations to gig workers and how they are treated.

Market Perception

Analysts believe that a certain saturation has set in the food delivery market, after the advent of quick commerce. Since its initial boom, quick commerce has cooled in many markets except India

Customer loyalty is dictated by whoever offers the cheapest price. Zomato & Swiggy compete through different membership offerings and promotion codes in food delivery. However, the offerings are dynamic, and with a priority to profitability, Swiggy is struggling (aggregate basis)

This also extends to quick commerce, with Blinkit waiving delivery charges on orders above INR 99, while Swiggy does it for orders above INR 199. This could see users gravitating towards Blinkit or Zept, both well-capitalized competitors

Is Swiggy Bloated?

Swiggy’s current value seems optimistic and more reflective of potential value in FY26.

With very little room for overvalued pricing Swiggy should seek a value at approximately 30-40% of Zomato’s valuation. This could result in interest from investors seeking value opportunities and potential oversubscription.

A successful IPO will still mean a year or more of losses for Swiggy. However, the market will reward Swiggy in terms of valuation multiples if they decide to go public and see an improvement in their operational margins & unit economics.

Zomato had set a precedent with the market punishing the Company for aggregate losses, especially when it acquired Grofers through a fire sale.

With food delivery plateauing, quick commerce offers significant growth opportunities in India due to unique factors such as a large unorganized retail sector, favorable demographics, and attractive unit economics.

Last week the industry witnessed major moves with Zepto gearing up to raise USD 650 Million in a reported pre-IPO round, and Zomato infusing INR 300 Crore in Blinkit.

With current competitors moving towards profitability, Swiggy Instamart is playing catch-up with possible break-even in a 2-year timeline. Strategic partnerships, cutting per-order costs, and elevating overall customer experience will result in improved quantifiable margins which could help Swiggy command a premium valuation in the future.

With increasing access and awareness, investors are now more conscious and active with their investments. I would love your opinion on this piece in the comments section!

This information is provided for informational purposes only and should not be considered investment advice. Always research or consult a financial advisor before making any investment decisions.

Bibliography:

inc42.com

the-ken.com

entrackr.com

reuters.com

economictimes.indiatimes.com

indiatoday.in

Great Insights. Quick commerce is changing the game.

Crazy content. Keep it up